Understanding US Healthcare Affordability: What Millions of Eligibility Checks Reveal About Patient Cost Exposure

Published:

November 12, 2025

Published:

November 12, 2025

When a patient asks "what will this cost?" at the front desk of a healthcare practice, the answer depends on a variety of factors. These include the procedure cost, multiple factors in the insurance plan structure, and the plan usage - complex and difficult for individual practices or patients to understand until the final bill comes back.

The need to understand healthcare costs is timely. As recent analysis from the New York Times reveals, Americans face premium increases of $66 to $920 per month if enhanced ACA subsidies expire at year-end - with the largest impacts hitting rural and older Americans. Beyond premiums, patients who secure coverage at manageable premium costs face a second, equally complex challenge: understanding what they'll actually pay when they need care. This is where our data provides useful insights.

Nirvana provides real-time eligibility verification and cost transparency solutions that help healthcare providers answer that question accurately, and it puts us in a unique position to observe what’s going on with healthcare affordability across the country. We process over 12 million eligibility transactions annually across multiple specialties and payer types, so we’re able to get a sense of both national trends in plan design and granular details (for example, how a single PPO plan change affects behavioral health coverage in rural Strafford County, New Hampshire). Learn more about our technology here.

Our data reinforces the basic understanding that variations in what patients pay across the U.S. can’t be pinned down to just one factor–like where someone lives, what their deductible is, or how concentrated its healthcare systems are. Instead, actual patient costs are shaped by a mulititude of factors, including deductibles, coinsurance rates, and out-of-pocket maximums, which interact to determine what people ultimately pay. This complexity often leaves patients confused about what they actually owe and hesitant to seek care they might otherwise get if costs were clearer and easier to understand.

While we have some visibility into these patterns, it's important to note that our data insights reveal some of the symptoms, but not the cause of the problem. The system's complexity comes from regulatory frameworks, market dynamics, employer purchasing decisions, and historical precedents. Our hope is that our data can contribute to the conversation around the rising cost of healthcare and help patients and practices understand the true cost of care.

For this piece, we’ve chosen to present the data on a state-by-state basis, showing the average across government and commercial plans within each state. This approach allows us to highlight national trends and patterns that we have observed. If you’re interested in more detailed, de-identified, plan-level data, please reach out to our team at support@meetnirvana.com

Patient cost exposure for any given medical procedure is determined by a combination of three plan design factors:

For example, take a $10,000 procedure. A patient might pay a $2,000 deductible, then 20% coinsurance on the remaining $8,000 ($1,600), for a total of $3,600 - unless their out-of-pocket maximum of $3,500 caps their responsibility first.

We refer to the $3,600 as the Total Patient Burden. The interplay between the three factors makes it challenging to focus on any one and draw any useful conclusions, so we’ll focus on Total Patient Burden to understand state-by-state variability to start.

Our analysis reveals that the average total patient burden for this identical procedure ranges from $2,280 in the lowest-cost state to $3,720 in the highest-cost state. That's a $1,440 difference in what a typical patient pays out of pocket, depending on which state they receive care in. For a patient managing ongoing behavioral health treatment, or a family budgeting for necessary imaging studies, this is a significant difference - it's the equivalent of several months of additional financial burden in one state versus another.

Now let’s shift to out-of-pocket maximums - the annual ceiling on patient financial responsibility. In the event patients have higher annual healthcare bills, the out-of-pocket maximum effectively becomes the Total Patient Burden, and is the best way to understand the patient’s cost of care. The average out-of-pocket maximum in each state ranges from $3,317 in the lowest-cost state to $7,227 in the highest-cost state in our dataset. For a family managing a chronic condition requiring multiple procedures throughout the year, or a patient facing a major health event, this $3,910 difference represents the gap between moderate financial strain and potentially catastrophic medical debt.

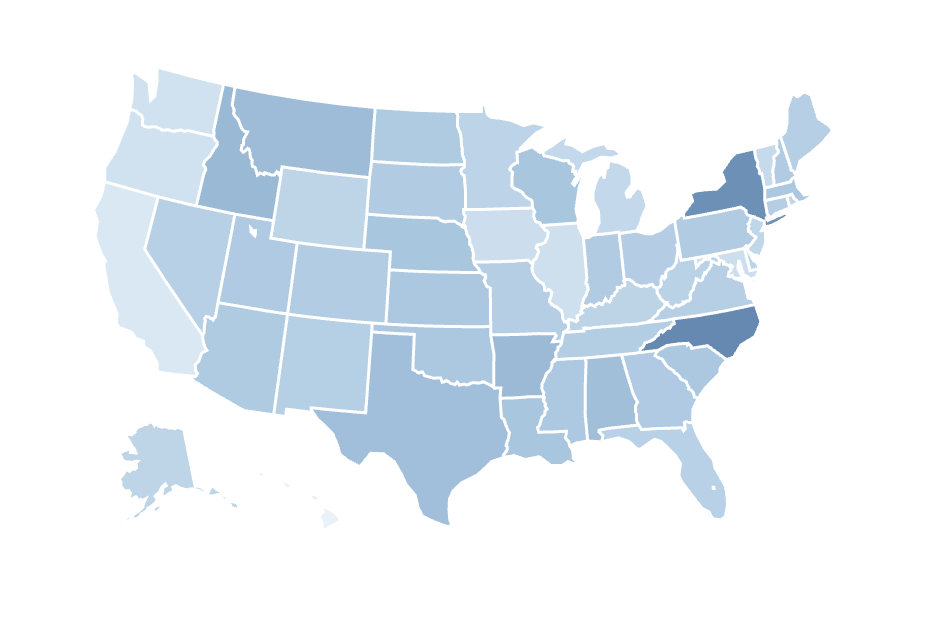

The state-level variation is also clear when examining each cost factor individually. Across our dataset, average deductibles for comparable plans range from $806 in Hawaii to $2,916 in Rhode Island—a gap of over $2,000 in what patients must pay before their coverage begins helping foot the bill for their medical treatment. Average coinsurance rates vary from 9.2% in New Mexico to 20% in North Carolina, meaning patients in some states continue paying more than twice the percentage of costs even after meeting their deductible. And average out-of-pocket maximums, as we saw earlier, span from $3,317 in Hawaii to $7,227 in North Carolina, setting vastly different ceilings on annual patient financial exposure.

Each state's insurance marketplace has evolved its own distinct combination, shaped by state regulations, insurer competition, employer purchasing decisions, and historical market dynamics. That results in a lot of idiosyncratic differences across states. For example, we observe that the average Rhode Island plan combines the highest deductible with moderate coinsurance rates. The representative average plan in North Carolina pairs high coinsurance with high out-of-pocket maximums, while Hawaii’s plans have low deductibles, low coinsurance, and low out-of-pocket maximums across the board.

To illustrate the magnitude of these differences more clearly, the charts below show the ten states with the highest and lowest patient costs under two scenarios: again, we show average total patient burden for a single $10,000 procedure, followed by average out-of-pocket maximums, which determine annual financial exposure for patients requiring ongoing or extensive care throughout the year.

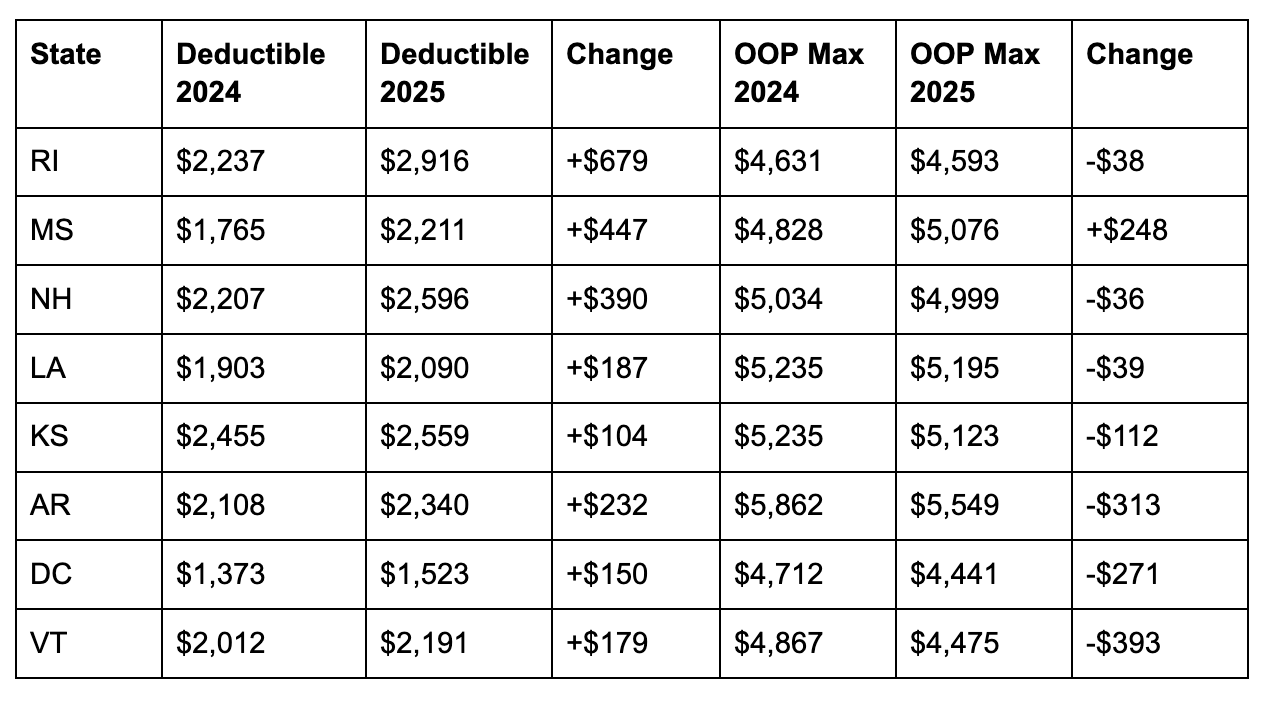

Our data also shows that the affordability landscape is shifting year-over-year, with meaningful changes between 2024 and 2025. Average deductibles increased by 8.4% year-over-year, from $1,885 to $2,043. At the same time, regulatory changes decreased the maximum out-of-pocket limits on average from $9,450 to $9,200 for individual coverage - a 2.6% reduction overall. The table below shows how deductible and out-of-pocket maximums changed between 2024 and 2025 in a selection of states.

These changes occurred alongside a restructuring of plan types. Traditional PPO plans have become unsustainable, with workers now paying 6% to 7% more for 2026 employer-sponsored health insurance—more than double the current rate of inflation. Our data shows measurable increases in HMO and POS enrollment between 2024 and 2025, with corresponding decreases in PPO plan selection. These restrictive plan types offer 20-30% lower premiums but feature narrower provider networks, required referrals, and reduced out-of-network coverage. The combination of higher deductibles and shifting plan types means that knowing a patient has coverage provides even less insight into their actual financial exposure than it did a year ago.

State-level variation creates very different financial journeys even in cases where total patient burden ends up being similar. A patient in a high-deductible, low-coinsurance state faces a significant upfront cost barrier, but once past that threshold, subsequent procedures become more manageable. A patient in a low-deductible, high-coinsurance state pays smaller initial amounts but continues facing substantial bills throughout the course of their treatment. States with mid-range values across all three factors produce moderate but unpredictable costs at each stage of care.

These differences shape treatment adherence, as well as the course of action a healthcare practice may recommend. A patient with a high deductible plan might delay starting treatment until they can afford the initial cost barrier, then maintain consistent appointments once the deductible is met. A patient with a high-coinsurance plan might begin treatment more easily but drop out mid-course as bills accumulate. In either case, financial uncertainty negatively impacts clinical outcomes. Both situations would be aided by cost transparency, or better yet - cost transparency coupled with value-based care models.

Given the complexities involved, knowing a patient has coverage provides limited insight into their financial exposure from a procedure. Patients need to know what they'll pay, when they'll pay it, and how that fits into their broader financial picture. Front desk staff need tools that deliver those answers in real-time, without adding administrative burden. Healthcare providers need operational intelligence that helps them maintain care access while managing revenue cycle complexity.

In today's healthcare landscape, cost transparency is a fundamental requirement for equitable access to care. The data we're tracking at Nirvana across millions of eligibility checks illustrates both the scale and complexity of the challenge. The trends emerging from our data mirror what external reports are signaling – plan complexity continues to increase, exacerbating the problem of hidden and unexpected healthcare costs. When patients understand their financial exposure upfront, they can make informed decisions about their care. And when practices have accurate cost information at the point of service, they can have meaningful conversations about treatment options and payment.

Navigating healthcare coverage and costs doesn't have to feel like wandering in the dark.

We're here to light the way.

.png)